$40.5 Billion in Climate Tech: What the 2025 Numbers Tell Us About 2026

Feb 24, 2026

A Market That’s Maturing, Not Slowing

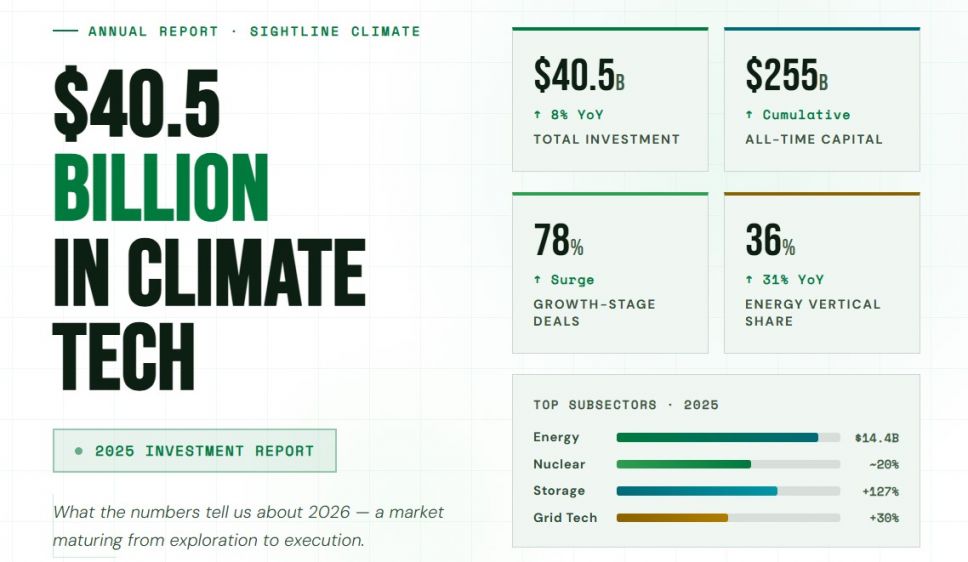

Global climate tech venture and growth investment hit $40.5 billion in 2025, according to Sightline Climate’s annual report. That’s an 8% uptick from 2024 and brings cumulative investment to $255 billion. On the surface, it looks like steady growth. Look closer, and a more nuanced picture emerges.

Deal count fell 18%. Early-stage seed and Series A totals both declined. Series C hit an all-time low in deal count. Meanwhile, growth-stage investment surged 78%, with average deal sizes climbing across the board.

This isn’t a market in retreat. It’s a market that has decisively shifted from exploration to execution.

Energy Is the Undisputed King

The energy vertical commanded 36% of all 2025 climate tech investment, growing 31% to $14.4 billion — a three-year high. Within energy, the hottest subsectors tell a clear story about where the world is headed:

- Energy storage is outpacing everything else. Sungrow reported 127% year-over-year growth in storage systems, with storage revenue surpassing inverter revenue for the first time in company history.

- Grid technology saw the Nasdaq’s main grid index outperform major stock indices with nearly 30% gains in 2025. As AI-driven data centers strain existing infrastructure, grid modernization has become one of the most investable themes in climate tech.

- Nuclear energy received approximately a fifth of all climate venture funding in the first nine months of 2025. In recent weeks alone, nuclear startups announced rounds totaling over $1 billion.

- AI-powered energy optimization is no longer a supporting tool but foundational infrastructure. Crusoe Energy raised $1.375 billion in Series E funding to power sustainable computing using stranded energy sources.

The Geography Shift

The US maintained its dominant position, with funding up 27%, driven by mega-deals in data centers, nuclear, and EVs. But the picture elsewhere is less rosy. European climate tech funding fell to $10.1 billion, its lowest level since 2020. MENA and Latin America both saw sharp declines.

For those of us working at the intersection of European and Middle Eastern markets, this decline isn’t just a problem — it’s an opportunity. Capital may be pulling back from these regions, but the underlying fundamentals — solar irradiance, hydrogen export potential, Vision 2030 infrastructure programs — remain extraordinarily strong. What’s missing isn’t opportunity; it’s investor-grade infrastructure: ESG reporting, regulatory alignment, bankable project documentation.

The New Investment Thesis

TechEnergy Ventures CIO Alejandro Solé captured the 2026 investment thesis in a single phrase: priorities are now speed first, cost second, clean third.

The AI race has fundamentally changed the calculus for large energy customers. Hyperscalers are spending $50-100 billion annually on infrastructure. They care less about how green the energy is and more about whether they can get enough of it fast enough to maintain competitive advantage.

But — and this is crucial — this doesn’t mean ESG doesn’t matter. It means ESG has shifted from a moral argument to a market access argument. CBAM, CSRD, and ISSB-aligned reporting in 40+ jurisdictions ensure that sustainability compliance remains non-negotiable for any company operating in or selling into regulated markets.

What This Means for Founders and Operators

Whether you’re building an energy storage startup, running a renewable energy project in the Gulf, or managing supply chains for grid equipment manufacturers, the message from 2025’s investment data is clear:

- The capital exists. Access depends on demonstrating commercial viability AND regulatory readiness.

- Geography matters. Europe and MENA need more investor-grade ESG infrastructure to compete with US capital attraction.

- Scale beats novelty. Investors want fewer, bigger bets on companies that can prove both performance and impact.

The energy transition is not slowing down. It’s growing up. And the companies that grow with it — with robust ESG frameworks, clear regulatory strategies, and bankable operational models — will capture a disproportionate share of the next $40 billion.